Analysis of the sales structure of passenger cars in the past three years

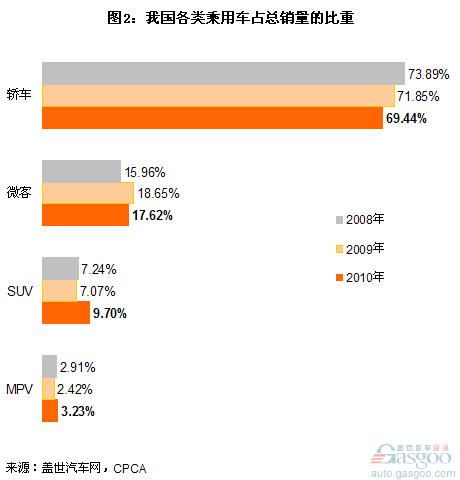

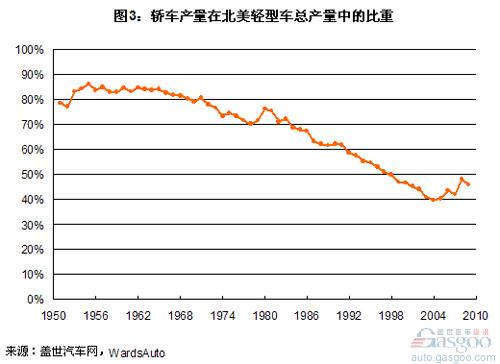

Note: The figures for 2009 and 2008 are sales for the same period of last year released in 2010 and 2009 respectively. Microbus and SUV led the 2009 and 2010 respectively, the car is always the main growth According to the data collected by Gasgoo.com, the sales volume of passenger cars in China in 2009 increased by 357,820 units year-on-year, of which the increase of 67.99% came from the car with the largest base, and the increase of 23.74% came from micro-customers. Sales of passenger cars and micro-customers increased by 48.59% and 78.53% year-on-year in that year, and micro-passenger growth ranked first among passenger cars. In 2010, passenger car sales increased further by 3,339,700, of which 62.10% were from cars, 17.72% from SUVs, and 14.49% from micro-customers. Sales of passenger cars and micro-customers increased by 28.35% and 25.48% year-on-year, respectively, while sales of SUVs increased by 82.20% year-on-year, which ranks first among passenger cars. The proportion of passenger cars in passenger cars continues to decline From the proportion of all kinds of cars in the total sales of passenger cars, the proportion of micro-customers with the fastest growth in 2009 increased by 2.69% to 18.65%. After the decrease in growth rate in 2010, its proportion in total sales of passenger vehicles also decreased by about 1 percentage point to 17.62%. The proportion of cars in the total sales of passenger cars has continued to shrink. In 2008, the proportion of passenger cars in the total sales of passenger cars was 73.89%, which was reduced by 2.04% in 2009 to 71.85%, and in 2010 it was further reduced by 2.41% to 69.44%. If we say that in the growing Chinese passenger car market, the decrease in the proportion of cars in 2009 was due to the high growth in sales and the relative increase in the proportion of micro-passenger sales. Therefore, the reduction in the proportion of cars in 2010 was mainly due to the high sales volume of SUVs. The relative increase in growth and weight. In 2010, the proportion of SUV increased by 2.63% year-on-year to 9.70%. Even when the micro-comparison ratio increased significantly in 2009, the proportion of SUVs in passenger cars was only reduced by 0.17%, and the decrease was smallest among passenger cars. MPV is still the smallest market for passenger cars in China. In 2009, its sales volume accounted for only 2.42% of the total passenger vehicle sales. Although it increased to 3.23% in 2010, it still sold only 444,400 units in the year. Future SUVs still have high growth potential, and the proportion of cars may be further reduced Micro-passenger as a crossover model, this is a niche market, its high growth in the first year of policy stimulus sales overdrafts and the lower growth in the second year, reflects its relatively low growth potential. After the withdrawal of stimulus policies in 2011, micro-customers will return to their normal growth rate, and because the previous two years have accumulated a higher base, this year's growth rate may further decline on the basis of 2010. The increase in sales of SUVs (most of which are more than 1.6L) is not due to the country's stimulus policy, but rather the release of its own growth potential. On the one hand, SUVs have won the favor of many second-time car buyers and even some first-time car buyers because of their larger interior space, sports and off-road performance, and more individual appearance and interior design. Its consumer demand is still relatively large, and its sales base is still small. This contradiction determines its future growth potential. On the other hand, major domestic car companies have already been and will further increase the launch of more competitive SUV models to promote market growth. The future SUV may further increase at a relatively high speed, and it is even expected to continue to lead the passenger car market for a certain period of time. With the acceleration of urbanization in China and the further release of potential consumption in the second and third tier cities and rural markets, the passenger car will continue to be the main driver of passenger vehicle growth for a longer period of time. However, its proportion in passenger cars will further decrease with the increase in the proportion of SUVs and other models. Compared to North America in mature markets, the proportion of cars in their light vehicles has been reduced from more than 80% in the 1950s and 1960s to less than 50% in this century (see Figure 3). Hollow Plate Welding Head,Medical Device Straight Circular Ultrasonic Fixture,Automotive Ultrasonic Straight Cylinder Mold,Ultrasonic Straight Cylinder Forming Die Changzhou Piling Automation Technology Co., Ltd. , https://www.plultrasonicmould.com

In 2009 and 2010, China's auto market showed blowouts. Unlike the blowouts caused by the first purchases by large numbers of consumers in first-tier cities around 2003, the blowouts mainly originated from the growth of first-time car purchases in second and third-tier cities and some rural consumers, and the second and second-tier cities The growth of car purchases.